The US Economy Remains As Resilient As Ever

Last week’s +1.8pt MoM advance in the ISM Services PMI (54.5 = 6mo high) was adequately presaged by the New York Fed’s Services Survey a couple of weeks ago. The New Orders PMI hit a 6mo high as well alongside the highest reading in the Employment PMI since Nov-21.

The probability of a near-term recession continues to dwindle because the services sector accounts for 86% of Total Nonfarm Payrolls.

Offsetting the positivity was the 4mo high in the Prices PMI, which is now trending higher again. If the inflation narrative devolves sooner than our qualitative research views anticipate, we could be in the early innings of a market crash.

China’s Crude Oil Imports accelerated to 30.9% YoY in August, fanning the flames of an ill-timed, hazardous breakout in energy prices.

All eyes on Wednesday’s August CPI report to confirm or disconfirm the prevailing “immaculate disinflation” theme, which itself is one-half of the “transitory GOLDILOCKS” theme we co-authored in mid-January (with the other being “resilient US economy”).

Will Bitcoin Crash Before The Halving?

Darius recently sat down with Anthony Pompliano to discuss global liquidity, bitcoin, the Fed, and more.

If you missed the interview, here are three takeaways from the conversation that have significant implications for your portfolio:

1. The Years Leading Up to Bitcoin Halvings Are Extremely Volatile.

When we analyzed the past Bitcoin halvings from November 2012, July 2016, and May 2020, we found that in the years leading up to the halving, Bitcoin tends to have three drawdowns of more than -20% on a median basis.

All drawdowns in the year leading up to halvings have a median decline of -27%.

We believe Bitcoin will be much higher in a few years, but it will likely require a rough path to reach its destination.

2. Over The Next Year, Liquidity Will Determine Bitcoin’s Path.

On a median basis, Bitcoin increases 144% in the year leading up to halvings.

These increases have closely followed global liquidity cycles; the liquidity cycle bottomed in 2012 and 2015, years leading into the halvings where Bitcoin increased 384% and 144%, respectively.

However, in 2019, when liquidity conditions were less favorable than in 2011 and 2015, Bitcoin failed to see a similar price increase.

The increase that year was only 20%, and the drawdowns were more significant than in the previous pre-halving years.

The amount of liquidity in asset markets will decide Bitcoin’s path over the next year.

3. We Believe The Fed Will Be Forced to Increase Their Inflation Target From 2% to 3%

The change will likely come in two phases:

- First, the market will become comfortable with inflation settling above 2%. This is likely a 2024-25 phenomenon.

- Then, when the unemployment rate is high enough, and with enough political pressure, the Fed will officially increase its target to 3%, ultimately paving the way for it to resume QE and lower interest rates. This is likely a 2025-26 phenomenon.

That’s a wrap!

If you found this blog post helpful:

- Go to www.42macro.com to unlock actionable, hedge-fund-caliber investment insights.

- RT this thread and follow @42Macro and @42MacroWeather.

- Have a great day!

All Things Macro

Darius recently sat down with Nick Halaris to discuss proper risk management, the labor market, inflation, asset markets, and much more.

If you missed the interview, here are three takeaways from the conversation that have significant implications for your portfolio:

1. Investors Are Doing A Great Disservice To Themselves By Not Being Bayesian

At 42 Macro, we use three core tenants to form our systematic macro risk management process:

- Regime Segmentation: We identify which investable regime the economy is in, the probability of that regime persisting, and how long it is likely to persist.

- Bayesian Inference: We systematically update the probability of relevant economic scenarios as new information becomes available to the market.

- Risk Management Tools: We use sophisticated quantitative tools like our Volatility Adjusted Momentum Signal (VAMS) and Global Macro Risk Matrix to predict when the price momentum of a particular security or overall market regime (risk on vs. risk off) is likely to change.

We urge our readers to infuse proper risk management in their investment strategies. We welcome you to use our tools if you want to gain a systematic edge in the market: https://42macro.com/sampleresearch.

2. Labor Hoarding Has Contributed To The Resilience Of The US Economy

The most recent US Total Labor Force SA reading was 167 million people – a value below its trendline since 2009.

Conversely, Gross Domestic Income recovered its trendline approximately 18 months ago and remains above it.

The discrepancy in strength between the two indicators suggests there is a large amount of cash in the economy that can be used to demand goods and services but insufficient labor to supply those goods and services.

3. History Tells Us The Fed Must Break The Economy to Achieve Its Price Stability Mandate

We analyzed every recession since 1969 and found that, on a median basis, core PCE inflation is almost always flat-to-up in the year leading up to a recession.

Historically, inflation does not break down without a recession.

Both this study and our HOPE+I framework confirm that inflation is a lagging indicator, and we believe it will again fail to fall below the Fed’s 2% target without a recession.

That’s a wrap!

If you found this blog post helpful:

- Go to www.42macro.com to unlock actionable, hedge-fund-caliber investment insights.

- RT this thread and follow @42Macro and @42MacroWeather.

- Have a great day!

What is Making the U.S. Economy so Resilient?

This week, Darius sat down with Maggie Lake from Real Vision to discuss the resiliency of the US economy, the housing market, and much more.

If you missed the interview, we have you covered. Here are three takeaways from the conversation that have significant implications for your portfolio:

1. The Resiliency of the US Economy Will Likely Continue

Our research shows the US economy has nowcast itself into “GOLDILOCKS” for the past five months. GOLDILOCKS is a regime marked by growth trending higher and inflation trending lower.

The strength of the economy will likely continue because:

- Goods demand is increasing — real goods PCE increased 5.4% on a three-month annualized basis in the most recent month.

- Corporations have been reducing inventories for the past five quarters, reducing 72 basis points off of GDP per quarter, on average. This, paired with increasing demand, could lead to inventory restocking the next few quarters.

2. New Home Sales Are Surging Because The Existing Home Sales Market Has Been Starved of Supply

Today, homeowners are unwilling to sell their homes and trade their ~3.5% mortgage (the effective mortgage rate nationally) for the current market rate of ~7%.

This supply shortage is causing a spike in new home builds:

- Building Permits are growing at 7% on a three-month annualized basis.

- Housing Starts are growing 31% on a three-month annualized rate of change basis.

- New Home Sales are growing at 21% on a three-month annualized basis.

3. “Bidenomics” Is Also Contributing to Our “Resilient US Economy” Theme

The US economy is experiencing a record non-war, non-recession budget deficit under the current administration.

Last year, the deficit was -3.7% of GDP.

Today, it is -8.4%.

That 470 basis point difference equates to approximately $1.3 trillion of incremental fiscal stimulus supplied to the US economy, further contributing to its resiliency.

That’s a wrap!

If you found this blog post helpful:

- Go to www.42macro.com to unlock actionable, hedge-fund caliber investment insights.

- RT this thread and follow @42Macro and @42MacroWeather.

- Have a great day!

Even Higher For Much Longer

Global bond yields hit their highest level since 2008 as investors were forced by the data we have been highlighting to reprice economic resiliency in places like the US and Japan, as well as sticky inflation in places like the Eurozone and UK.

Last week’s Industrial Production (+210bps to a 2mo high 3mo SAAR of -0.9% in July), Capacity Utilization (+70bps to a 2mo high of 79.3% in July), Building Permits (+590bps to a 3mo high 3mo SAAR of 7.1% in July), Housing Starts (+2,560bps to a 2mo high 3mo SAAR of 30.9% in July), and NY Fed Services Activity Survey (+0.6pts to 0.6 in August; highest since Sep-22) were each marginally confirming of our “resilient US economy” theme.

Market participants are increasingly accepting the “higher for longer” guidance we have seen from a handful major central banks — most notably the Federal Reserve.

Floor policy rate expectations (min value on OIS curve out 2yrs) for the ECB, Fed, and BOE have climbed +3bps, +39bps, and +37bps MoM, respectively.

That’s dragged 10yr Nominal German Bund, US Treasury, and UK Gilt Yields up +18bps, +48bps, +37bps, respectively, over that same duration.

The 10yr Nominal JGB Yield — which is effectively managed by the BOJ — is even up +22bps MoM.

China’s Structural Liquidity Trap Rears Its Ugly Head

The economic situation in China continues to be an unmitigated disaster, with the July Retail Sales, Industrial Production, and Fixed Assets Investment all slowing and missing consensus estimates.

Animal spirits in China are being weighed down by beleaguered private sector balance sheets. With respect to liabilities, China remains one of the most indebted major economies in the world. With respect to assets, China’s property market — the #2 asset for Chinese citizens behind bank deposits — has yet to recover from the beating it took from the 1-2 punch of “Zero COVID” and Emperor Xi’s “Three Red Lines” macroprudential policy.

All told, the Chinese economy is doing exactly what we thought it would do in the absence of large-scale fiscal stimulus — i.e., return to the structural liquidity trap it was mired in prior to COVID.

What Is The Outlook on Inflation?

Earlier this week, Darius joined Anthony Pompliano to discuss Global Liquidity, Inflation, the Housing Market, and more.

In case you missed it, here are five takeaways from the interview every investor needs to see:

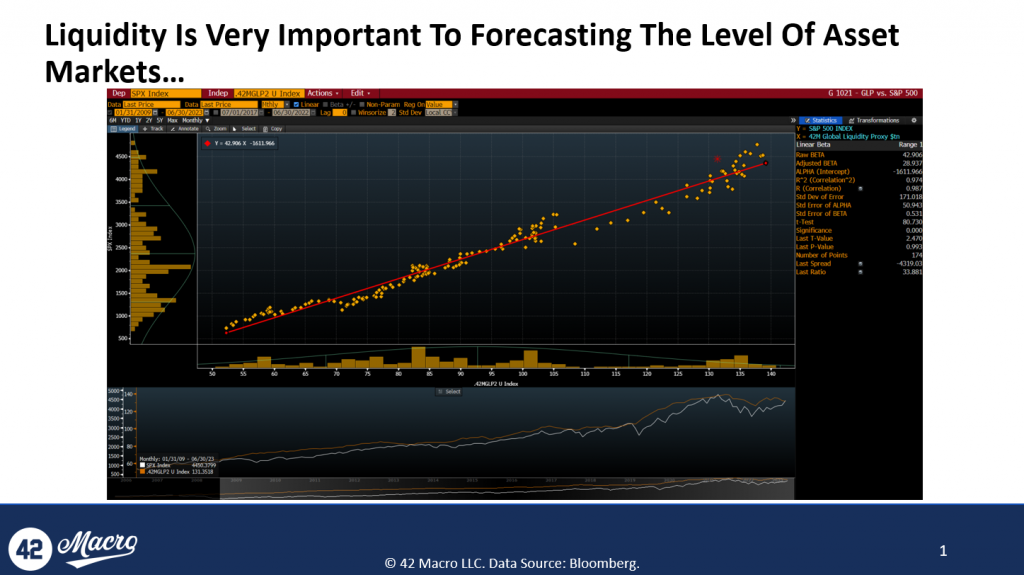

1. Global Liquidity Has Been Declining Over The Past Few Months

Our proxy for global liquidity, estimated via central bank balance sheets, broad money supply, and FX reserves minus gold, has been waning over recent months.

Now that we have observed a negative inflection in global liquidity, it is important for investors to ascertain the durability of this nascent trend.

2. Liquidity And Asset Markets Are Correlated On A Levels Basis, But Not On A Rate of Change Basis

The correlation between global liquidity and the S&P500 is substantial on a level basis, explaining 97% of the index’s level since 2009.

However, when regressing global liquidity against the rate of change of the S&P500, there is only a 12% correlation between the two.

When analyzing Bitcoin, we found that liquidity explains 77% of its level but 0% of its rate of change.

So, although liquidity is essential to understanding the long-term trend in asset markets, we should not linearly extrapolate its effects on asset markets in the short to intermediate term.

3. Inflation Will Be The Driver That Causes Asset Markets to Decline

We believe the revival of inflation as an important topic could lead to a downturn in the markets.

Currently, we are seeing favorable inflation outcomes and growth exceeding expectations supporting asset markets.

This dynamic has been beneficial for asset markets in H1, and we believe it will continue through July and possibly into August.

However, we might see inflation data harden afterward, especially relative to consensus expectations.

As the market begins to acknowledge that inflation will be sticky and require more global policy tightening than has been priced in, we expect a market correction.

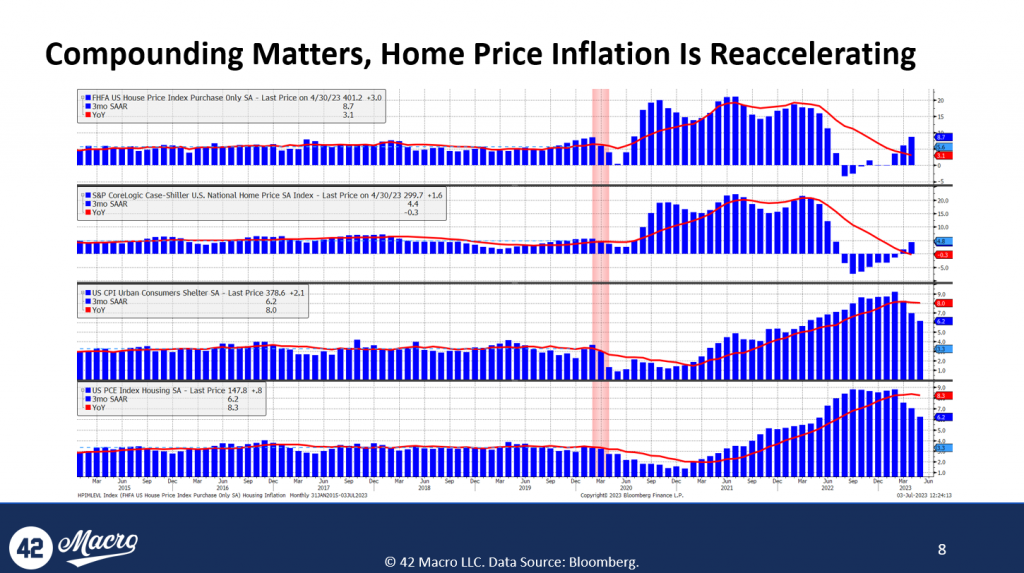

4. Home Prices Are Reaccelerating

According to the FHFA home prices index, home prices are increasing at a rate of 8.7% on a three-month annualized basis after bottoming in the first half of the year.

There is a rising probability we will see housing inflation bottoming out in the next two to three quarters, but at levels that contradict the Fed’s 2% inflation mandate.

The implications of this trend could be concerning, as the Fed might need to do significantly more to counteract the inflation impulse from the housing market.

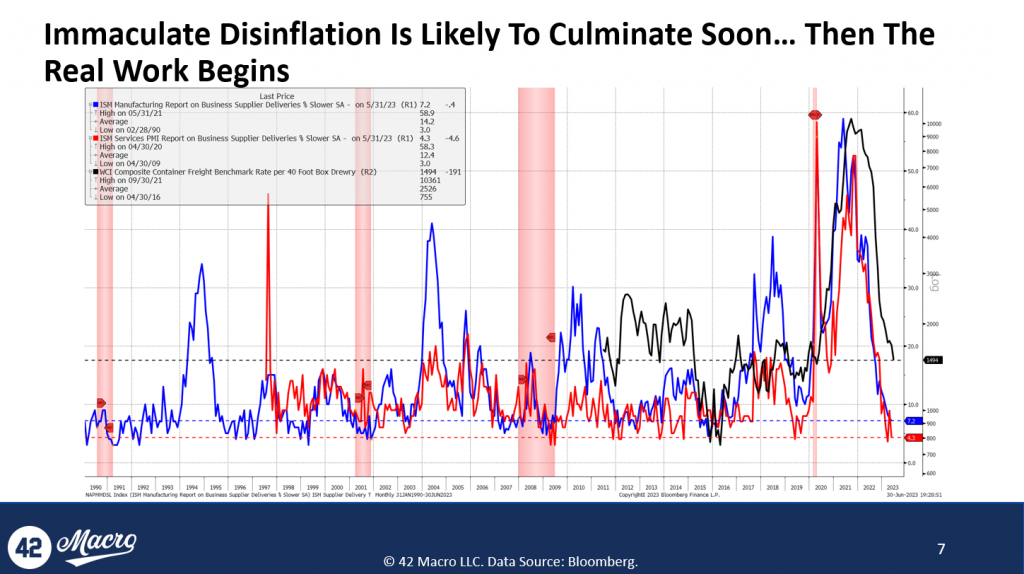

5. The Days of Immaculate Disinflation Are Over

Indices like ISM manufacturing, ISM services, and the supply delivery times index are back at levels consistent with 2% inflation, implying that the period of “immaculate disinflation” driven by pandemic-related factors is coming to an end.

We believe that the easy part of the inflation battle might be over soon.

That’s a wrap!

If you found this thread helpful, go to www.42macro.com/appearances to unlock actionable, hedge-fund caliber investment insights.

Macro Outlook

Darius joined Benjamin Cowen from Into The Cryptoverse earlier this week to discuss Inflation, the Labor, Liquidity, and more.

If you missed the interview, we have you covered. Here are three key insights that are important for your portfolio:

1) Despite The Recent Dovish Print on Inflation, We Believe The Fed Will Hike At The July Meeting

The money markets are currently pricing in approximately an 80% probability that the Federal Reserve will hike at their next meeting.

Generally, the Fed tends to move in sync with asset markets, acting according to what the market has priced in.

However, the Fed’s decisions are not purely inflation-oriented; they take into account labor market conditions as well.

Given these indicators, we believe the Fed will likely push through with the rate hike come July’s meeting.

2) Labor Hoarding Is Contributing to The Resiliency of The U.S. Economy

While the US Total Labor Force SA is trailing behind the pre-pandemic 2009-2019 trend, we have seen the Gross Domestic Income regain the trend shortly after the pandemic concluded.

This disparity tells us that there is an abundance of money in the economy but an inadequate labor force to meet the demand for goods and services.

Additionally, since March 2020, we have experienced labor demand outpace supply, with a staggering 3.9 million more in demand compared to available labor.

This excess demand for labor is causing labor hoarding, further strengthening the resilience of the U.S. economy.

3) We Are In A Liquidity Cycle Upturn; The Global Liquidity Cycle Bottomed In Fall of Last Year

Our 42 Macro Global Liquidity proxy, a sum of global central bank balance sheets, global broad money supply, and global FX reserves minus gold, shows a declining trend in recent months.

However, we believe the liquidity cycle bottomed last fall, and we are currently in the midst of a likely 2.5-year upswing.

Although we may see some turbulence over the next few quarters, Bitcoin, in this environment, could perform exceptionally well, pushing it above the $100,000 level by the end of next year.

In between now and then, we still anticipate a recession will commence in the US economy in the next two to three quarters, likely causing risk assets to fall as the Phase 2 credit cycle downturn sets in – a scenario that we believe has not been priced into the market yet.

We continue to believe risk assets will squeeze higher and peak in Q4 or Q1 of next year.

#respectthexaxis

That’s a wrap!

If you found this thread helpful, go to www.42macro.com/appearances to unlock actionable, hedge-fund caliber investment insights and have a great day!

What’s Propping Up The US Consumer?

Last week, Darius joined Maggie Lake from Real Vision to discuss Rate Hikes, Inflation, the Stock Market, and more.

In case you missed it, here are five takeaways from the interview every investor needs to know:

1) The Market Believes The Fed Is Done Hiking. We Are Fading That View.

Currently, money markets are pricing in the assumption that future inflation data will force the Fed to pause at their July meeting.

Moreover, money markets are pricing in twice as much easing over the next two years by the Fed as they are the ECB (Fed: ~200 basis points; ECB: ~100 basis points)

We believe this is unlikely because 1) the European economy is already in recession, and 2) the European inflation cycle tends to lag the US by two quarters; as a result, they are heading into the most disinflationary part of their Inflation Cycle in 2H23.

While it may not occur in July due to a likely dovish June CPI release, we expect the Fed to continue to raise rates in the coming months.

Consequently, we foresee the dollar grinding higher over the medium term.

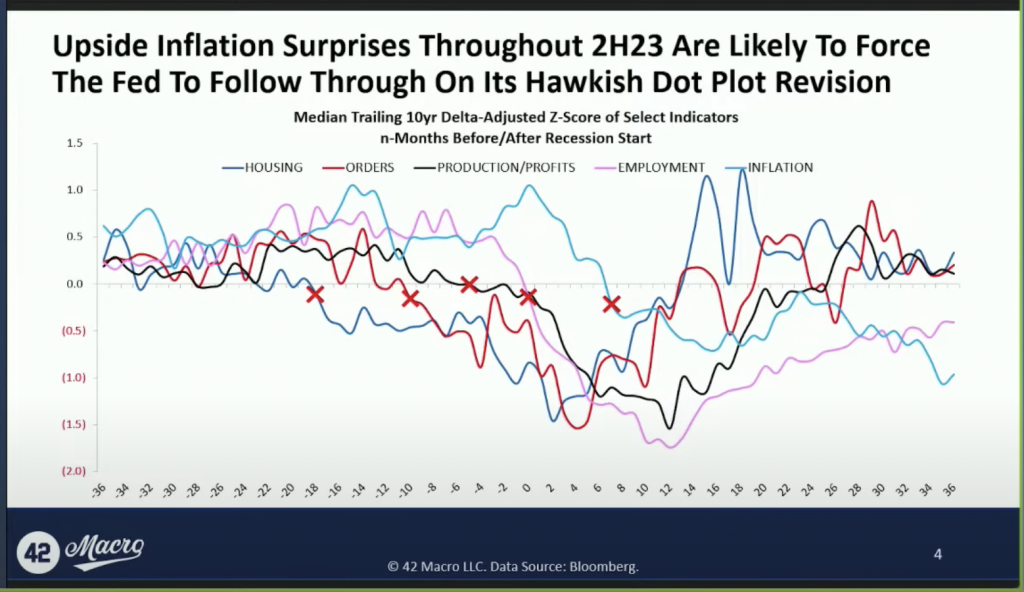

2) We Expect A Series of Upside Inflation Surprises Throughout 2023

Throughout the year, erroneous forecasts have caused investor consensus to roll forward the recession starting point; now, consensus estimates call for the recession to begin in Q3.

However, inflation tends to break down 6-8 months after the recession starts – it is the most lagging indicator of the US Business Cycle.

As a result, we believe we will not see any further significant disinflation after the June CPI release without a substantial drawdown in the labor market.

3) A Variety of Factors Are Propping Up The Consumer

We are seeing a wide range of conditions still propping up the US consumer:

- Unemployment is still low; the booming US labor market has allowed consumers to continue spending

- Cash on household and corporate balance sheets is high, currently at 3% of total assets. The last time that ratio was that high was in the 1960s

- Manufacturing as a % of GDP has declined substantially in recent decades. That is important because manufacturing tends to account for 98% of total job loss during recessions. Now only 18% of GDP, this more volatile sector of the economy is a much smaller percentage of total employment too at only 14%.

- Housing is resilient; despite the interest rate increases, outstanding mortgage rate debt is still at 3%. There is a standstill in existing home sales because consumers will not trade lower mortgage rates for the higher current rates – this has increased demand for new homes, thus holding up the housing market.

4) The Phase 2 Credit Cycle Downturn Is Ahead of Us

We believe the recession is still ahead of us.

Since the Great Depression, EVERY recession has had a market crash associated with it as we price in the downturn in the credit cycle.

In addition, on a median basis, markets tend to peak a month before the lowest point in the unemployment rate.

So, we typically see degradation in the labor market and a dip in the stock market simultaneously.

That means investors who share our longer-term (6-12mos) bearish outlook for the stock market must avoid expressing that view with actual trades until we are much closer to the start of recession. Since last fall, we have identified 4Q23 as the quarter with the highest probability of seeing a recession commence in the US economy. The second highest probability is 1Q24.

5) The Stock Market Is Likely Nearing A Local Top

This stock market rally has caught many investors off-guard; most fund managers are hastily rushing to minimize their YTD underperformance.

As a result, the rally can largely be explained by investors chasing the market higher, further squeezing Bears.

Despite the recent uptrend, we advise against chasing stocks now.

We expect a correction in the near term for a variety of fundamental (e.g., declining US and global liquidity) and technical (e.g., the passage of a large, call-heavy OPEX should reverse flows) reasons.

That’s a wrap!

If you found this thread helpful, go to www.42macro.com/macro-bundle to unlock actionable, hedge-fund caliber investment insights and have a great day!

Macro Indicators and Tactics for Uncertain Times

1) The US Economy Remains on a Path to a Recession

At the beginning of the year, most investors expected a first-half recession followed by a recovery in the second half.

Since last summer, our view has consistently been that the U.S. economy had more endurance than what was perceived by most investors.

This belief led us to forecast a later start to the recession, in late-2023, contrary to the general market consensus.

Our view was, and still is, that a recession would likely kick off in Q4 of this year or Q1 of next year.

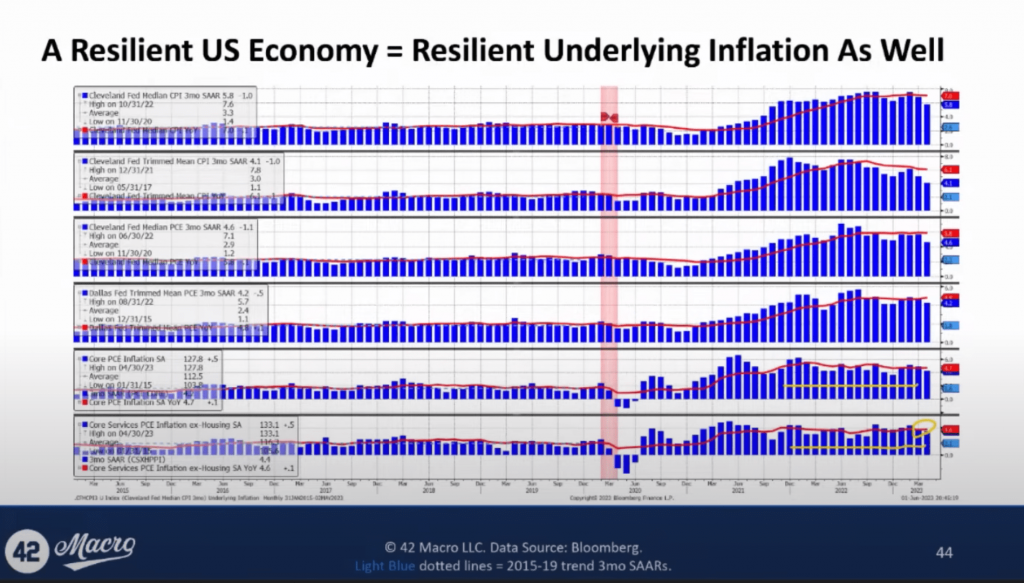

2) Inflation Will Not Reach 2% Without a Recession

U.S. inflation, a lagging business cycle indicator, usually breaks down during and through a recession.

Our data suggests that it’s improbable we will see evidence of sustainable 2% inflation before a recession hits: our models currently forecast inflation stabilizing at around 3-5%, not the Fed’s 2% target.

This could lead to two potential outcomes: either the Fed acknowledges more action is needed, or the bond market panics over the lack of progress.

Either way, we believe it will result in the Fed applying more pressure, pushing the economy into recession.

3) Europe’s Economic Contraction Will Likely Worsen

The European economy has recently confirmed its recession, primarily due to the effects of monetary tightening.

Despite the assumptions that fiscal stimulus would resolve the situation, Europe’s economy is in decline, with retail sales tracking down 2% to 4% across Europe.

Given the current data, we predict the recession in Europe is likely to worsen over the medium term.

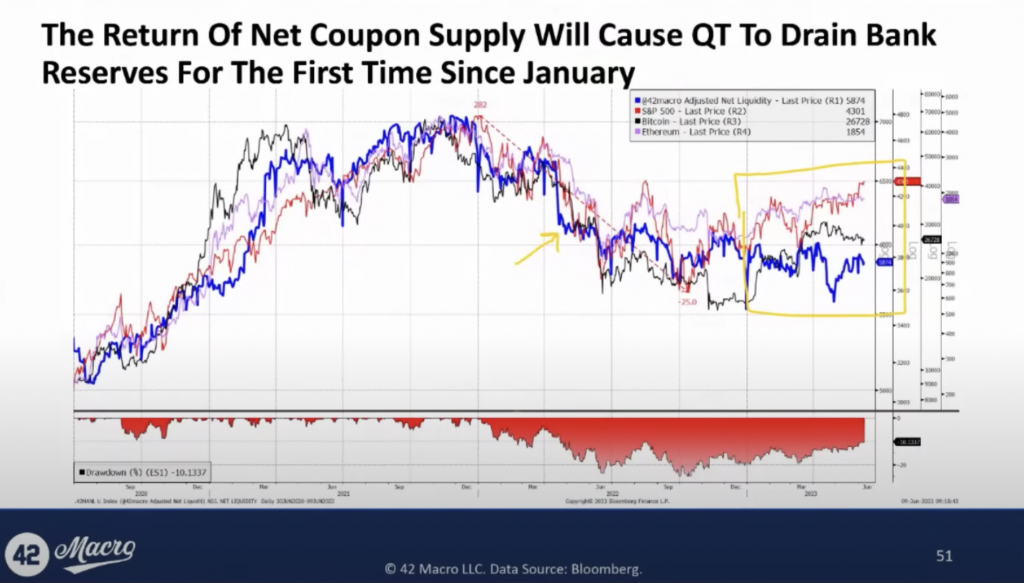

4) Upcoming Quantitative Tightening Will Negatively Impact Asset Markets

The return of net coupon supply will instigate QT, causing it to deplete bank reserves for the first time since January.

Our Adjusted Net Liquidity model, which subtracts the Treasury General Account (TGA) balance and Reverse Repo Facility (RRP) balance, as well as emergency lending from the Fed’s balance sheet, shows a breakdown in the correlation between US public sector liquidity and asset markets at the beginning of the year when QT ceased draining bank reserves.

Up until now, QT has truly been going on in the background.

We believe this correlation will resume in the coming months and negatively affect risk assets.

5) The Stock Market Is Likely To Peak During Q4 (or Early In Q1 At The Latest)

Our study of past recessions shows that the stock market, on a median basis, typically peaks a month before the trough in the unemployment rate.

Historically, the stock market usually rises sharply in the year leading up to the end of a business cycle, with a median return of around +16%.

Equity markets are generally strong preceding a recession.

We maintain the view that the stock market will likely peak in Q4 (or early in Q1 at the latest) and many of today’s too-early bears will fail to profit from the pending Phase 2 Credit Cycle downturn.

At that point, we will be positioning for the next anticipated down leg in the market.

That’s a wrap!

If you found this thread helpful, go to www.42macro.com/macro-bundle to unlock actionable, hedge-fund caliber investment insights and have a great day!