Welcome to The Weekly!

Recent divergence in global equity markets reflects mounting scrutiny of corporate AI capex trajectories, as market participants parse both escalating investment commitments and the deflationary risk AI poses to non-technology industry profits.

From this starting point, bank deregulation appears to be a greater upside risk than AI disruption is a downside risk, as (1) regulators broadly align on a deregulatory trajectory tied to the recalibration of the US Basel III Endgame framework, and (2) Paradigm C—the growth phase of the cut → grow → print sequence required to address the geopolitically driven supply-demand imbalance in the Treasury bond market continues to be the dominant driver of the economy and asset markets.

Elsewhere, the Q4 GDP and December PCE data supports our Resilient US Economy, U-Shaped Economy, and Sticky Inflation themes, broadly aligning with the latest FOMC projections of a ~2% real growth and 2.5–3.0% inflation US economy.

In Case You Missed It

This Is What Kevin Warsh Will Say About the Labor Market to Fix the Fed’s Broken Reaction Function

Enjoy this excerpt from our February 14, 2026 | Around the Horn webcast breaking down the declining dynamism of the US labor market as indicated across dozens of key high- and low-frequency economic statistics.

Our research continues to view the Fed’s reluctance to return the policy rate to a neutral setting as perpetuating a likely jobless recovery. Additionally, we project a structural uptrend in productivity growth, which will likely cause an even greater bifurcation between the outlooks for GDP and corporate profitability and the outlooks for employment, consumer confidence, and incumbent politicians.

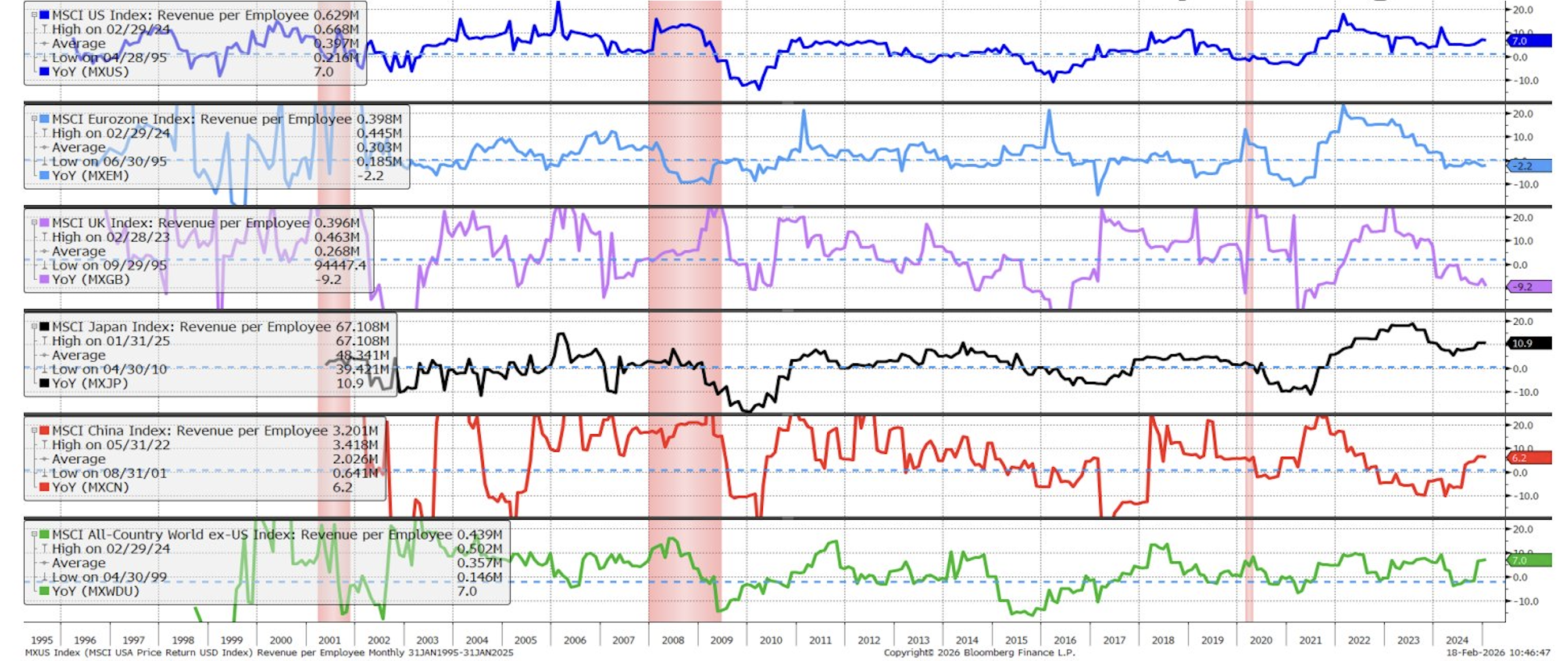

Chart of the Week

The Diffusion of AI Throughout The Global Economy Favors International Stocks Over US Stocks As Productivity Converges

As AI adoption spreads across the global economy, productivity gains are broadening beyond the U.S. While U.S. firms have led in recent years, the convergence of global productivity trends suggests international equities may be positioned to benefit as AI-driven efficiency gains become more evenly distributed across developed and emerging markets.

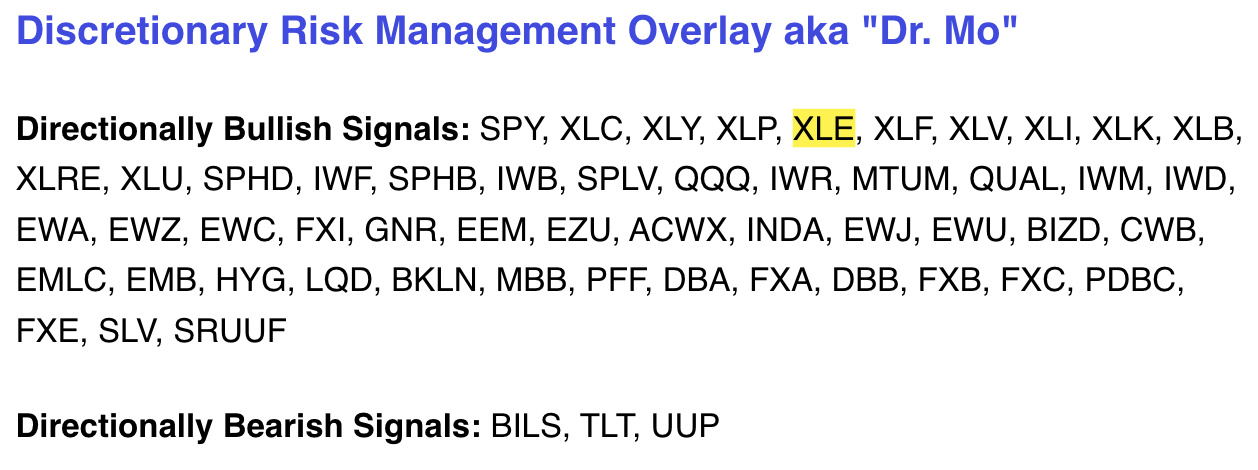

Successful Signals From Dr. Mo

On November 29th, 2025, our Discretionary Risk Management Overlay signaled a bullish breakout in Energy $XLE. Since the pivot, $XLE has appreciated 21%.

Community Spotlight

This week, we’re excited to share feedback from a member of our global investor community. Specifically, the data-driven discipline that 42 Macro provides to our community.

It’s always rewarding to see KISS and Dr. Mo deliver meaningful outcomes for investors around the world. We truly appreciate your feedback.

Parting Shot | Factor Risk

Market risk is one thing. Factor risk is another.

Staying on the right side of the cycle is difficult. Staying on the right side of growth vs. value, U.S. vs. international, quality vs. beta, across multiple rotations, is exponentially harder.

Factor rotations occur more frequently than market cycles. The probability of stacking consistent wins declines dramatically.

Most investors don’t need factor alpha. They need disciplined exposure to beta and systematic risk management.

Explore 42 Macro’s KISS and Dr. Mo and discover the frameworks and signals that underpin our systematic approach to managing risk.

EXPLORE 42 MACRO RESEARCH