Last week, Darius joined Maggie Lake from Real Vision to discuss Rate Hikes, Inflation, the Stock Market, and more.

In case you missed it, here are five takeaways from the interview every investor needs to know:

1) The Market Believes The Fed Is Done Hiking. We Are Fading That View.

Currently, money markets are pricing in the assumption that future inflation data will force the Fed to pause at their July meeting.

Moreover, money markets are pricing in twice as much easing over the next two years by the Fed as they are the ECB (Fed: ~200 basis points; ECB: ~100 basis points)

We believe this is unlikely because 1) the European economy is already in recession, and 2) the European inflation cycle tends to lag the US by two quarters; as a result, they are heading into the most disinflationary part of their Inflation Cycle in 2H23.

While it may not occur in July due to a likely dovish June CPI release, we expect the Fed to continue to raise rates in the coming months.

Consequently, we foresee the dollar grinding higher over the medium term.

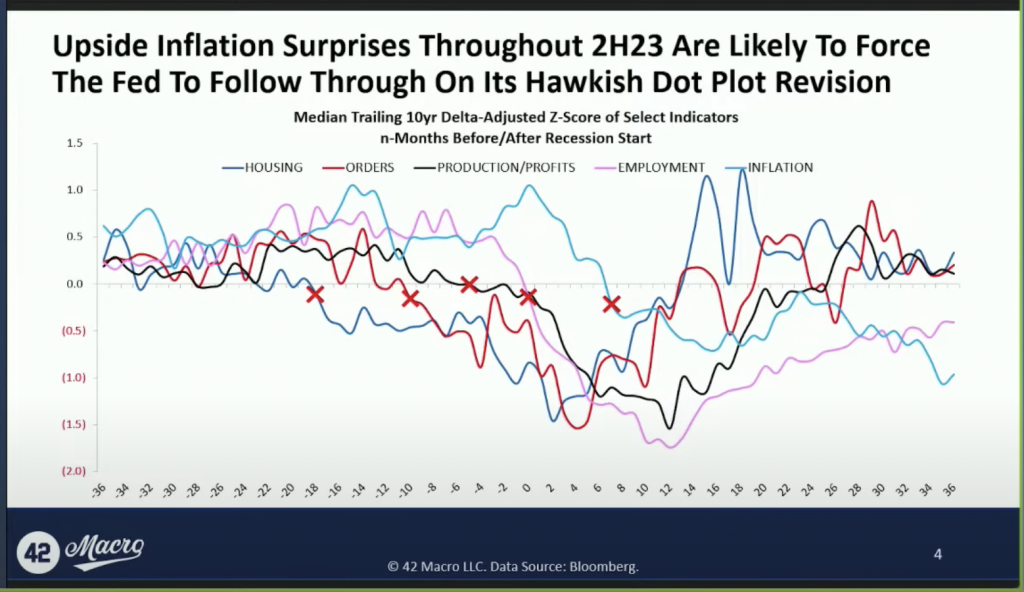

2) We Expect A Series of Upside Inflation Surprises Throughout 2023

Throughout the year, erroneous forecasts have caused investor consensus to roll forward the recession starting point; now, consensus estimates call for the recession to begin in Q3.

However, inflation tends to break down 6-8 months after the recession starts – it is the most lagging indicator of the US Business Cycle.

As a result, we believe we will not see any further significant disinflation after the June CPI release without a substantial drawdown in the labor market.

3) A Variety of Factors Are Propping Up The Consumer

We are seeing a wide range of conditions still propping up the US consumer:

- Unemployment is still low; the booming US labor market has allowed consumers to continue spending

- Cash on household and corporate balance sheets is high, currently at 3% of total assets. The last time that ratio was that high was in the 1960s

- Manufacturing as a % of GDP has declined substantially in recent decades. That is important because manufacturing tends to account for 98% of total job loss during recessions. Now only 18% of GDP, this more volatile sector of the economy is a much smaller percentage of total employment too at only 14%.

- Housing is resilient; despite the interest rate increases, outstanding mortgage rate debt is still at 3%. There is a standstill in existing home sales because consumers will not trade lower mortgage rates for the higher current rates – this has increased demand for new homes, thus holding up the housing market.

4) The Phase 2 Credit Cycle Downturn Is Ahead of Us

We believe the recession is still ahead of us.

Since the Great Depression, EVERY recession has had a market crash associated with it as we price in the downturn in the credit cycle.

In addition, on a median basis, markets tend to peak a month before the lowest point in the unemployment rate.

So, we typically see degradation in the labor market and a dip in the stock market simultaneously.

That means investors who share our longer-term (6-12mos) bearish outlook for the stock market must avoid expressing that view with actual trades until we are much closer to the start of recession. Since last fall, we have identified 4Q23 as the quarter with the highest probability of seeing a recession commence in the US economy. The second highest probability is 1Q24.

5) The Stock Market Is Likely Nearing A Local Top

This stock market rally has caught many investors off-guard; most fund managers are hastily rushing to minimize their YTD underperformance.

As a result, the rally can largely be explained by investors chasing the market higher, further squeezing Bears.

Despite the recent uptrend, we advise against chasing stocks now.

We expect a correction in the near term for a variety of fundamental (e.g., declining US and global liquidity) and technical (e.g., the passage of a large, call-heavy OPEX should reverse flows) reasons.

That’s a wrap!

If you found this thread helpful, go to www.42macro.com/macro-bundle to unlock actionable, hedge-fund caliber investment insights and have a great day!